- Apr 12

Estate Planning Glossary: Clear Terms for Confident Decisions

- Marla Landa

- Estate Planning

Join our Newsletter for More Good Stuff!

Understanding your estate plan shouldn’t require a law degree. This glossary breaks down the most important terms in plain language so you can plan ahead with clarity and confidence.

These aren’t legal definitions. They’re real-world explanations designed to help you understand what you’re signing, who’s doing what, and how it all fits together.

Whether you’re creating a new plan or making updates after a life change, these terms will help you feel more confident as you move forward.

Key Terms to Know (A–Z)

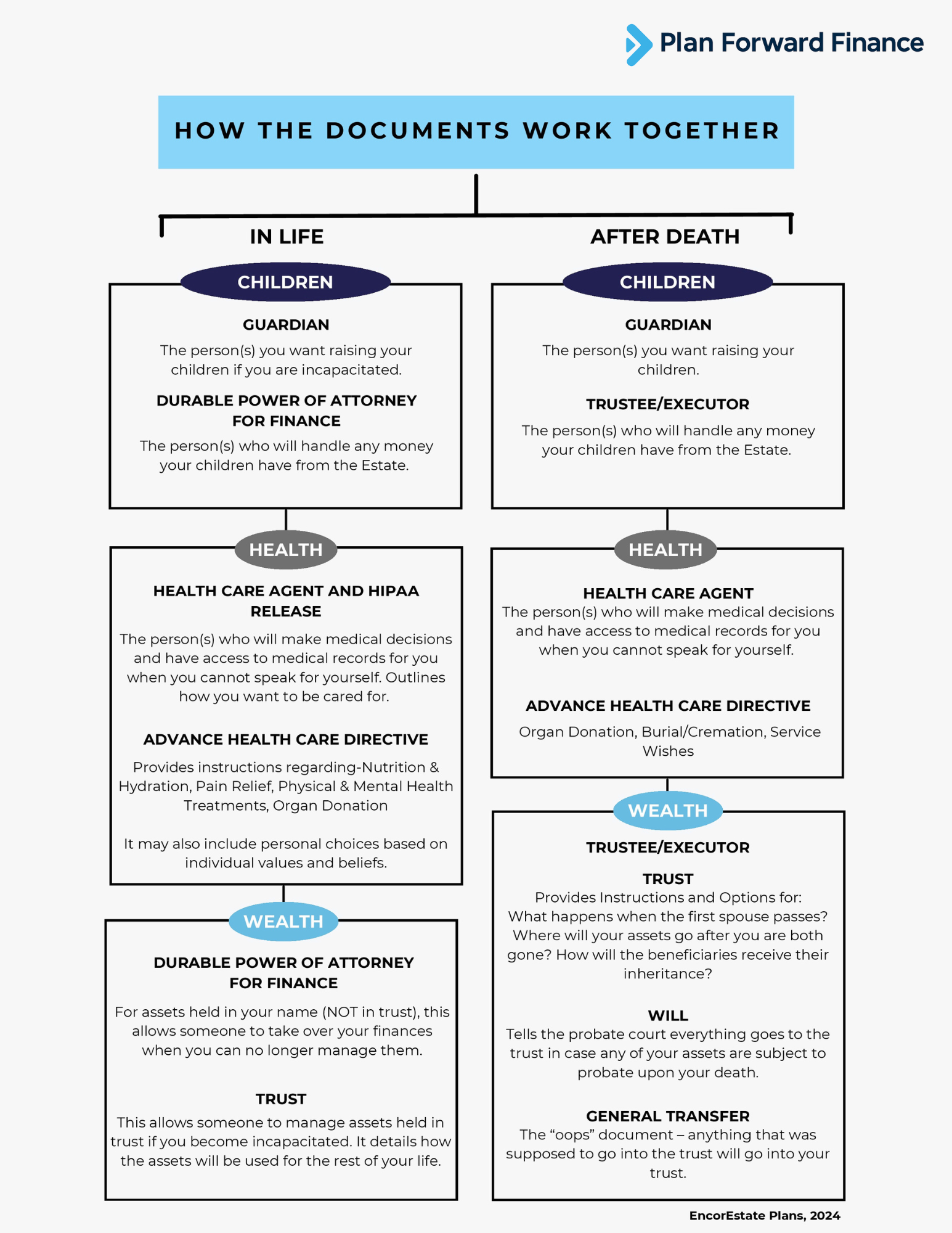

Advance Health Care Directive

Also known as a directive to physicians, health care declaration, or medical directive. This document lets you communicate your wishes about medical care if you can’t speak for yourself. It often covers both life-prolonging treatments and end-of-life care. Think of it as a written instruction manual for your doctors, outlining what kind of care you do or don’t want if you’re ever unable to communicate your preferences.

Affidavit (Self-Proving Affidavit)

A sworn, written statement executed under oath in front of a witness or witnesses. The witness(es), upon their signing, may also be attesting to the affiant's state of mind and the absence of cohesion or duress during execution.

Affidavit of Domicile

A sworn, written statement verifying a deceased person’s legal residence, usually at the time of death. It is often used when transferring certain assets after death.

Affidavit of Survivorship

A sworn, written statement used to confirm that one joint owner has passed away and to establish the identity of the surviving owner, often for the purpose of transferring title to jointly held property.

Agent

A person authorized to act on your behalf under a legal document, such as a financial power of attorney, medical power of attorney, or advance healthcare directive.

Asset

Anything an individual, family, or business owns that has value, such as cash, property, or investments.

Beneficiary

The person or organization you name to receive your assets after you pass away. It’s important to review these designations regularly, especially on retirement accounts and life insurance policies, to make sure they reflect your current wishes.

Buy-Sell Agreement

A buy-sell agreement is a legal contract between business co-owners that explains what happens if one owner dies, becomes disabled, retires, or wants to leave the business. It helps prevent unexpected buyers from stepping in and ensures the remaining owners have a plan for buying out the departing owner’s share. It often includes how the business will be valued and how the purchase will be funded. This can help reduce confusion, conflict, and surprises.

Capacity

Your ability to understand and make decisions when signing legal documents. You must have capacity when you create your estate plan.

Child/Children

The biological or legally adopted offspring of a person. In many estate planning contexts, the term may include children of one or both spouses. A “child” often refers to someone who is under the age of majority, which is typically 18, though this can vary by state or country.

Claim or Claims Against an Estate

Demands made by a decedent’s creditors to collect unpaid debts from the estate. These claims are generally addressed during the probate process and are typically paid before any remaining assets are distributed to heirs or beneficiaries.

Codicil

A formally executed document used to amend or update an existing Will without needing to rewrite the entire document.

Community Property

A type of joint ownership for married couples (and in some cases, registered domestic partners) where most assets acquired during the marriage are considered owned equally by both spouses, regardless of who earned or purchased them. This includes income, real estate, and other assets accumulated while married.

These rules can affect how assets are divided in a divorce and how they pass through your estate at death. If you live in a community property state, it’s important to understand how your assets will be classified and distributed in your Will or Trust.

Community property laws apply in Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. Alaska also allows couples to opt in to a community property arrangement.

Contingent Beneficiary

A person named to receive benefits under a Will, Trust, or other arrangement if the primary beneficiary is unable or unwilling to receive them.

In insurance policies, a contingent beneficiary receives the benefit if the primary beneficiary cannot.

Corporate Trustee

A professional trustee, typically a bank, trust company, or investment firm, hired to manage and administer a trust. Corporate trustees are often chosen for their experience, continuity, and ability to remain impartial, and they are bound by fiduciary duties to follow the terms of the trust.

Corporate trustees are usually compensated based on a percentage of the trust’s assets, often ranging from about 0.5% to 2% annually. While this can be more expensive than naming a family member or friend, it provides professional management and reduces the risk of personal bias or conflict.

Custodian

A person who holds and manages property for the benefit of another, similar to a trustee. Custodians are most commonly used to hold assets for minors, who are not legally able to manage property on their own.

Under laws such as the Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA), adults can transfer assets such as money, securities, or insurance to a custodian, who holds and manages the property for the minor’s benefit.

Custodians are fiduciaries and are required to act in the best interest of the beneficiary.

Decedent

An individual who has passed away.

Descendant

A person who is directly descended from another, such as a child, grandchild, or great-grandchild. In estate planning, this includes all lineal descendants across generations.

Disinherit

To intentionally exclude a person, often a natural heir, from receiving a share of an estate.

Durable Power of Attorney (POA)

This document allows the agents you name to act on your behalf and make financial decisions if you become unable to do so. The word “durable” means it stays in effect if you’re incapacitated.

Estate

Everything you own at the time of your death, including your home, bank accounts, investments, and personal belongings.

Executor

The person you name in your will to carry out your wishes, settle debts, and distribute your assets.

General Transfer (or General Assignment)

A simple document that moves your untitled personal property into your Revocable Living Trust. It acts as a catch-all for things that don’t have a formal title, like furniture, art, clothing, or tools.

It helps ensure these items are included in your Trust, even if they aren’t listed individually.

Covers: furniture, clothing, jewelry, collectibles, and other untitled items

Does not cover: real estate, bank accounts, vehicles, or business interests

Including a General Transfer strengthens your estate plan and helps your loved ones avoid probate for personal belongings.

Guardian

Someone you appoint to care for your minor children or dependents if something happens to you.

HIPAA Release

HIPAA stands for the Health Insurance Portability and Accountability Act, a federal law passed in 1996 to protect your medical records and personal health information. A HIPAA release allows the people you choose to speak with your doctors and access your medical records if needed.

Intestate

Dying intestate means passing away without a valid will. When this happens, your state’s intestacy laws determine how your assets are distributed after any debts are paid. Usually, this means your closest living relatives inherit, but exactly who qualifies depends on your state and your family situation.

If you don’t have a will, the court decides who gets what. That can lead to delays, added stress for your loved ones, and outcomes that might not match what you would have wanted.

Key Person Insurance

Key person insurance is a life or disability insurance policy a business takes out on a crucial team member such as a founder, executive, or top-performing employee. If that person passes away or becomes seriously ill, the payout helps the business cover lost income, hire and train a replacement, or manage other financial needs. It is one more way to protect the business from uncertainty.

Lapse

Lapse occurs when someone named in your Will or Trust dies before you and no alternate is listed. Their gift “lapses,” meaning it fails or gets redistributed. What happens next depends on how your estate plan is written and whether your state has an “anti-lapse” law. Some states pass the gift to the deceased person’s descendants. Others divide it among the remaining beneficiaries.

Lapse is not the same as per capita, but it can lead to a similar result if no backup or other distribution method (like per stirpes) is named.

Letter of Wishes

Also called a memorandum of wishes. This is a personal letter to your trustees explaining your intentions and goals for the trust. It is not legally binding, but it can be very helpful in guiding decisions. It doesn’t need to be written by a lawyer. A simple typed or handwritten letter is often enough.

Living Will

A living will is not about your stuff. It’s a legal document that explains your wishes for medical treatment if you become unable to speak for yourself. This includes choices about life support, resuscitation, and other types of care at the end of life.

Living Trust

A living trust is a specific type of trust that you set up while you’re still alive. It is revocable, which means you can change or cancel it at any time. You’re typically the trustee and the beneficiary while you’re living, so you stay in full control. A living trust helps:

Avoid probate

Keep things private

Plan for incapacity

Make things smoother for your loved ones

Non-Probate Assets

Assets that pass directly to a named beneficiary without going through probate. Common examples include retirement accounts, life insurance policies, and property owned jointly.

Notary

A person authorized by the state to witness the signing of important documents and verify the identity of the people signing them. In estate planning, certain documents like a trust, power of attorney, or deed transfer may need to be notarized to be legally valid. Having something notarized helps prevent fraud and confirms that the signatures are authentic. Think of a notary as an official witness who adds an extra layer of protection and trust to your important paperwork.

Per Capita

Per capita is a method of inheritance distribution that means “by head.” It divides the estate equally among all living beneficiaries at the same generation level. If a beneficiary dies before you, their share is divided among the surviving beneficiaries at that level—not their children.

Example: If you have three children and one dies before you, the remaining two each receive half. The deceased child’s kids do not inherit anything.

Per Stirpes

Per stirpes is a method of inheritance distribution that means “by branch.” It keeps the inheritance within the family line. If a beneficiary dies before you, their share goes to their descendants.

Example: If you have three children and one dies before you, leaving two children of their own, that one-third share would be split between your two grandchildren.

Pour-Over Will

A will that “pours over” any assets not already in your revocable trust into the trust when you pass away. It acts as a safety net to make sure everything is handled the way you intended.

Power of Attorney – Finances

A Power of Attorney for Finances allows you to name someone you trust to manage your financial affairs if you are unable to do so yourself due to illness, injury, or incapacity.

This person, known as your agent or attorney-in-fact, can handle tasks such as paying bills, managing bank accounts, filing taxes, or making financial decisions on your behalf.

It only applies during your lifetime and can be customized to take effect immediately or only if you become incapacitated.

Power of Attorney – Health Care

Also known as a medical power of attorney or health care proxy. This document allows someone you trust to make medical decisions on your behalf if you are unable to speak for yourself.

This person, called your health care agent or proxy, can talk with your doctors, access medical records, and make real-time choices based on your preferences and best interests.

It works alongside your Advance Health Care Directive:

The directive outlines your wishes

The power of attorney names the person who makes sure those wishes are understood and respected

Both documents are essential to making sure your voice is heard, even when you cannot speak for yourself.

Probate

The legal process of validating your will and distributing your estate through the court system. It can be time-consuming, expensive, and public, which is why many people create trusts to avoid it.

Revocable Trust

Also known as a living trust or inter vivos trust. This type of trust lets you manage your assets during your lifetime and decide what happens to them after you pass away. It avoids probate for anything inside the trust. A revocable trust can be individual (for one person) or joint (for a couple).

Succession Plan

A succession plan is a thoughtful strategy for keeping your business running smoothly when you are no longer at the helm. It outlines who might take over key roles, how they will be prepared, and what steps to follow during a planned or unexpected transition. A good plan can help preserve your legacy, avoid disruption, and give your team and loved ones peace of mind about the future of the business.

Title

Refers to who legally owns an asset. For example, if your name is on a home’s title, you are the legal owner of that property.

Trust

A trust is a legal arrangement where you (the trustor) transfer ownership of your assets to a trust, which is managed by a trustee for the benefit of one or more beneficiaries. Trusts can provide more control, privacy, and flexibility than a will. Trusts are often used to avoid probate or manage how and when beneficiaries receive assets. There are many types of trusts, and each one serves a specific purpose.

Trust Certification (also known as a Certificate of Trust)

A short summary of your trust that proves its existence and shows who your trustees are. It is commonly used when you need to work with banks or other institutions without showing them your full trust document.

Trustee

The person or institution you name to manage your trust. They are responsible for following the instructions you have outlined in your trust document.

Trust Funding

The process of transferring assets into your trust. This includes retitling property like real estate or accounts so that they are owned by the trust. Without proper funding, your trust may not function as intended. It’s a good idea to periodically review your assets to ensure they are properly titled.

Will

A legal document that outlines who should receive your property after your death and who should care for any minor children. If you have a trust, your will still plays an important role in naming guardians and covering anything not held in the trust. Note that this is NOT the same as a "Living Will."

Why It Matters

One of the most common mistakes in estate planning is making things too complex. A clear, simple set of core documents, paired with a letter of wishes and good communication, can go a long way toward meeting your goals and giving your loved ones peace of mind.

Two things to keep in mind:

Fund your trust. An unfunded trust won’t help you avoid probate.

Review your beneficiaries. Keep them up to date to avoid surprises.

We’re not here to scare you into action. We’re here to help you make thoughtful, informed choices with clarity and confidence.

Let’s Make a Plan That Works for You

This glossary is just the beginning. If you’re ready to create or update your estate plan, we’re here to guide you every step of the way.

Thanks for reading :)

Marla @ Plan Forward Finance